A private home equity mortgage is rarely going to be a borrower’s first choice for financing. Private mortgages involve fees and extraordinary costs that you wouldn’t typically pay through a more conventional institutional mortgage lender like your bank.

However, private home equity mortgage lenders serve an incredibly important purpose for Canadian homeowners to unlock equity built up in their home that would otherwise be inaccessible.

You might be wondering what makes a private or home equity lender so different than an institutional lender.

At its core, the answer has to do with how each type of lender approaches the 5 Cs of credit:

Your institutional lenders are looking for the crème de la crème in each of the 5 Cs with very little leniency or flexibility if a borrower doesn’t fit into the box. This strict lending criteria can marginalize borrowers and lead them to have to deal with pricier home equity loan options.

WHY ARE BANKS SO TIGHT vs. PRIVATE EQUITY LENDERS?

If you’re reading this, chances are you’ve been to your bank and are probably frustrated that they won’t make an exception to approve your mortgage even though you have a terrific real estate asset that continues to go up in value.

There are two overarching reasons why banks and institutional lenders won’t make exceptions for you:

- REGULATION: Banks and lenders are governed by multiple governmental organizations, the largest one of which is the Office of the Superintendent of Financial Services (OSFI). One of the foundations of any modern economy is a stable banking and financing system. If banks were not regulated in terms of what how they can and cannot lend, then you can risk collapsing the whole system. Don’t believe me? Just look up the cause of the 2008 Financial Crisis for a reminder.

- CONSISTENCY: investors and managers alike of banks and institutional lenders want predictable consistent measured returns without volatility. The enemy of predictable consistency is discretion and exceptions on their tight lending guidelines.

But to say that borrowers who don’t meet the tight guidelines of banks and institutional lenders are not worthy is to throw the baby out with the bath water!

PRIVATE HOME EQUITY MORTGAGE LENDERS TO THE RESCUE

Private mortgage lenders consist of individuals or groups of individuals who will pool money together to lend. From a private home equity mortgage lender’s point of view, a loan is an investment opportunity secured on real estate.

However to believe that private home equity mortgage lenders will throw money at you just because you own a house is completely wrong.

Like banks and institutional mortgage lenders, a private lender will still consider the 5 Cs of credit, however they will be more willing to make exceptions and pursue opportunity to earn a higher interest rate on their mortgage loan.

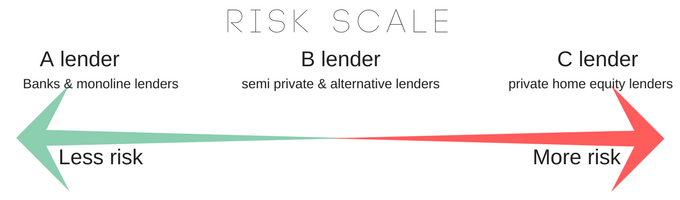

THE RISK SCALE

A very simple concept to understand. The lower the risk, the lower the rate and pricing for financing. As you move up the risk scale the more expensive your financing options will be.

DO YOUR HOMEWORK

If you find yourself in a situation where you need a private home equity mortgage loan, do your homework. Find out where you fit in along the risk scale and where the cut offs are for each type of lender – A, B, C etc…

I would recommend speaking with more than one mortgage broker because based on their experience and relationships they may be able to place you with a suitable private home equity mortgage lender to minimize fees and extra expenses.

Let’s get in touch. You can contact me here or book a call into my calendar below.